The Portuguese Supreme Administrative Court ruled in favour of taxpayers. The Portuguese Tax Authority refused to accept its ruling. The lower courts became divided. And taxpayers were left caught in the middle—uncertain whether they should pay, whether they could recover the tax, or simply whether they were being treated fairly.

Imagine your father passes away and leaves a property to four siblings. None of them wishes to keep the property. They decide to sell it. They pay capital gains tax because “that’s what everyone does.”

But was it actually required?

The answer, which for years appeared obvious, no longer is—and it may entitle taxpayers to reclaim tax that should never have been paid.

What Is an Undivided Estate—and Why Does the Distinction Matter?

When a person dies and the heirs have not yet formally partitioned the estate, the estate remains undivided. Each heir is entitled to a share of the estate as a whole—known under Portuguese law as a quinhão hereditário (inheritance share)—but none of them individually owns any specific asset comprised within the estate.

This legal distinction has an important consequence that, for many years, the Portuguese Tax Authority failed to recognise: if no heir owns a specific immovable property before the estate has been partitioned, how can the transfer of that legal position be taxed as the disposal of a real right over immovable property?

The Portuguese Tax Authority’s answer was straightforward: because it could. And for many years, that approach prevailed.

The Core Issue

The Portuguese Personal Income Tax Code (Código do IRS) provides for the taxation of capital gains arising from the disposal for consideration of rights in rem over immovable property. The central legal question is therefore whether an inheritance share constitutes a right in rem over immovable property.

For many years, the Portuguese Tax Authority maintained that it did.

The Portuguese Supreme Administrative Court has now held otherwise.

The Judgment That Changed Everything—and the Tax Authority Turned a Blind Eye

In April 2025, the Portuguese Supreme Administrative Court delivered Judgment No. 7/2025, a judgment for the harmonisation of case law (acórdão de uniformização de jurisprudência)—the highest form of judicial precedent in Portuguese tax litigation—which established the following principle:

“The disposal of an inheritance share does not constitute the disposal for consideration of rights in rem over immovable property. Accordingly, any gains arising from such disposal are not subject to Personal Income Tax (IRS).”

Supreme Administrative Court, Judgment for the Harmonisation of Case Law No. 7/2025, 29 April 2025.

The Court’s reasoning is as straightforward as it is devastating for the Tax Authority’s position: while the estate remains undivided, an heir holds a share in an autonomous pool of assets rather than a right over any specific property. Consequently, there is no right in rem over immovable property capable of being transferred and, therefore, no taxable capital gain for Personal Income Tax purposes.

What happened next was unexpected.

Rather than applying the decision of the highest court within the administrative jurisdiction, the Portuguese Tax Authority issued binding administrative guidance adopting the opposite interpretation.

It continued to levy tax.

An Unprecedented Stand-Off

This has given rise to an unprecedented situation.

The highest court within the administrative jurisdiction has settled the legal position through a judgment harmonising case law. The Tax Administration has declined to follow it. The lower courts have reached conflicting decisions.

Taxpayers have been left in the middle—without certainty and, in many cases, paying tax that may not have been lawfully due.

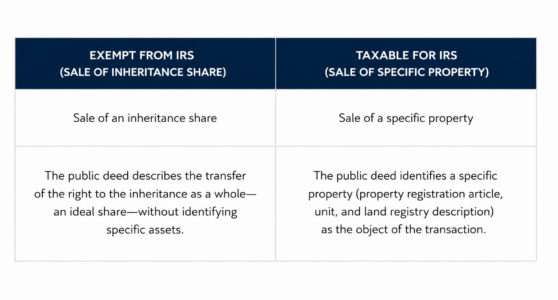

Following Judgment No. 7/2025, the Portuguese Tax Authority did not retreat. Instead, it issued Circular Letter No. 20281/2025, partially acknowledging the Supreme Administrative Court’s decision while introducing a distinction that, in practice, substantially limits its scope.

Two transactions that are economically identical—where heirs transfer their interests to a purchaser before the estate has been partitioned—may receive entirely different tax treatment solely because of the manner in which the notary drafted the deed.

The difficulty is that most Portuguese taxpayers who sold property belonging to an undivided estate did so by executing a deed for the sale of a specifically identified property, because that is the standard practice.

It is precisely those transactions that the Portuguese Tax Authority continues to tax.

The Battle of the Courts—Where Matters Become Even More Complex

If you thought that Judgment No. 7/2025 had settled the issue once and for all, think again.

In February 2026, the South Central Administrative Court (Tribunal Central Administrativo Sul) delivered a judgment limiting the scope of the Supreme Administrative Court’s harmonising case law and ruled in favour of the Portuguese Tax Authority. According to that decision, where the heirs dispose of a specifically identified immovable property, the transaction constitutes a disposal for consideration of immovable property for all relevant tax purposes, and the resulting gain remains subject to Personal Income Tax (IRS). In other words, the decisive factor is the wording of the public deed.

However, in December 2025, the Supreme Administrative Court went a step further. It dismissed an appeal brought by the Portuguese Tax Authority, which sought to challenge the very case law previously established by the Court, even though the transaction had been formally described as the sale of a specific property.

The Supreme Administrative Court’s position is unequivocal: the legal and economic substance of the transaction prevails over its formal characterisation.

“The Appellant [the Portuguese Tax Authority], being under a duty to pursue the public interest and unable to disregard the position adopted by the Supreme Administrative Court in the aforementioned judgment harmonising case law […], it is difficult to understand why it has chosen to ignore that position entirely in the arguments it has advanced.”

Supreme Administrative Court Judgment No. 0136/25.5BALSB, 17 December 2025.

The practical consequence is a profound degree of legal uncertainty.

Depending on the court—and, in some cases, depending on the individual judge—the very same taxpayer carrying out the very same transaction may obtain entirely different outcomes.

Can I Recover the Tax I Have Already Paid?

This is undoubtedly the question of greatest practical importance for taxpayers who have already sold their inheritance interests.

The honest answer is: perhaps—but it depends on a number of factors that must be assessed on a case-by-case basis.

What can safely be said is that taxpayers who have paid Personal Income Tax (IRS) on capital gains arising from the disposal of inheritance shares—or from the sale of assets forming part of an undivided estate—now have strong legal grounds for seeking reimbursement of that tax, relying on Judgment No. 7/2025 of the Supreme Administrative Court.

The Portuguese Tax Authority has already begun to accept certain applications for review.

Not all, however.

Moreover, strict statutory time limits apply.

The time limits for challenging tax assessments or seeking repayment of tax unduly paid are not unlimited and vary according to the circumstances of each case, including the tax year concerned, whether a tax return was filed, whether an additional assessment was issued, and other relevant procedural factors.

In some cases, those deadlines may already be approaching expiry.

Taxpayers should therefore seek advice without delay.

What If I Have Not Yet Sold?

If you are planning to sell property forming part of an undivided estate, the manner in which the transaction is structured and documented may determine whether—or not—you become liable to pay a substantial amount of Personal Income Tax (IRS).

The wording of the public deed, the legal characterisation of the transaction, the composition of the estate, the number of heirs involved, whether the estate includes additional assets, and a range of other factors may all affect the applicable tax treatment.

There is no universal answer.

There is only the correct answer for the particular circumstances of each case.

The Good News

Unlike the position that existed only a few years ago, there is now clear guidance from Portugal’s highest administrative court in favour of taxpayers.

Those who carefully structure the transaction before the public deed is executed—rather than attempting to resolve matters afterwards—are in a far stronger position to benefit from this important development in Portuguese tax law in a secure and legally robust manner.

In Summary: What Has Changed, What Has Not, and What Nobody Yet Knows

What has changed

The Portuguese Supreme Administrative Court has adopted a clear and authoritative position: the disposal of an inheritance share is not subject to Personal Income Tax (IRS).

Taxpayers who have already paid tax may have legal grounds to seek repayment.

Those planning to dispose of assets forming part of an undivided estate should ensure that the transaction is appropriately structured from the outset.

What has not changed

The Portuguese Tax Authority has not altered its administrative practice.

It continues to tax transactions where the public deed identifies a specific immovable property as the object of the sale.

The South Central Administrative Court has endorsed that approach.

What nobody yet knows

It remains unclear whether the Portuguese legislature will intervene, when such intervention may occur, and what its scope will be.

It is uncertain whether Parliament will codify the interpretation adopted by the Portuguese Tax Authority or instead enshrine the position taken by the Supreme Administrative Court.

It is equally unclear whether any future legislative amendment will have retroactive effect or how it will affect pending disputes.

For the time being, only one conclusion is certain:

Every case turns on its own facts, statutory deadlines continue to run, and failing to act may prove costly.

For more information or specialized assistance, click here to schedule a meeting with one of our professionals.

The content of this information does not constitute any specific legal advice; the latter can only be given when faced with a specific case. Please contact us for any further clarification or information deemed necessary in what concerns the application of the law.